The 401(k) Default Trap

Most Americans never touch their 401(k) settings. Not once. They enroll—or get enrolled—choose a contribution rate, pick an investment allocation, and then… nothing. For years. Sometimes decades.

This isn't procrastination in the traditional sense. It's something more structural, more predictable, and significantly more expensive. It's the default trap, and it's costing American workers hundreds of thousands of dollars in retirement savings they'll never recover.

The Architecture of Inaction

Here's what happens: You start a new job. During orientation, HR explains the 401(k). You're automatically enrolled at a 3% contribution rate. Your money goes into a target-date fund matched to your approximate retirement year. You nod, sign the form, and get back to learning where the coffee machine is.

Years pass. You get raises. You change apartments. You get promoted. You never touch that 3%.

Ninety-three percent of employees who are auto-enrolled remain in the plan regardless of the default contribution rate. Not 93% who stay enrolled—93% who never change anything. Eighty percent do nothing, even at the highest contribution rates.

This isn't a personal failing. It's a design outcome.

The Pension Protection Act of 2006 cleared the legal path for employers to automatically enroll workers in 401(k) plans. The idea was sound: shift retirement saving from an active choice to a passive default, leveraging behavioral inertia to boost participation. It worked spectacularly. Automatic enrollment adoption has more than tripled since year-end 2007, and participation in auto-enroll plans can reach 94%, compared with 64% in voluntary enrollment plans.

But behavioral inertia is a double-edged knife. The same psychological force that gets people into the plan keeps them locked at whatever rate the plan administrator picked for them.

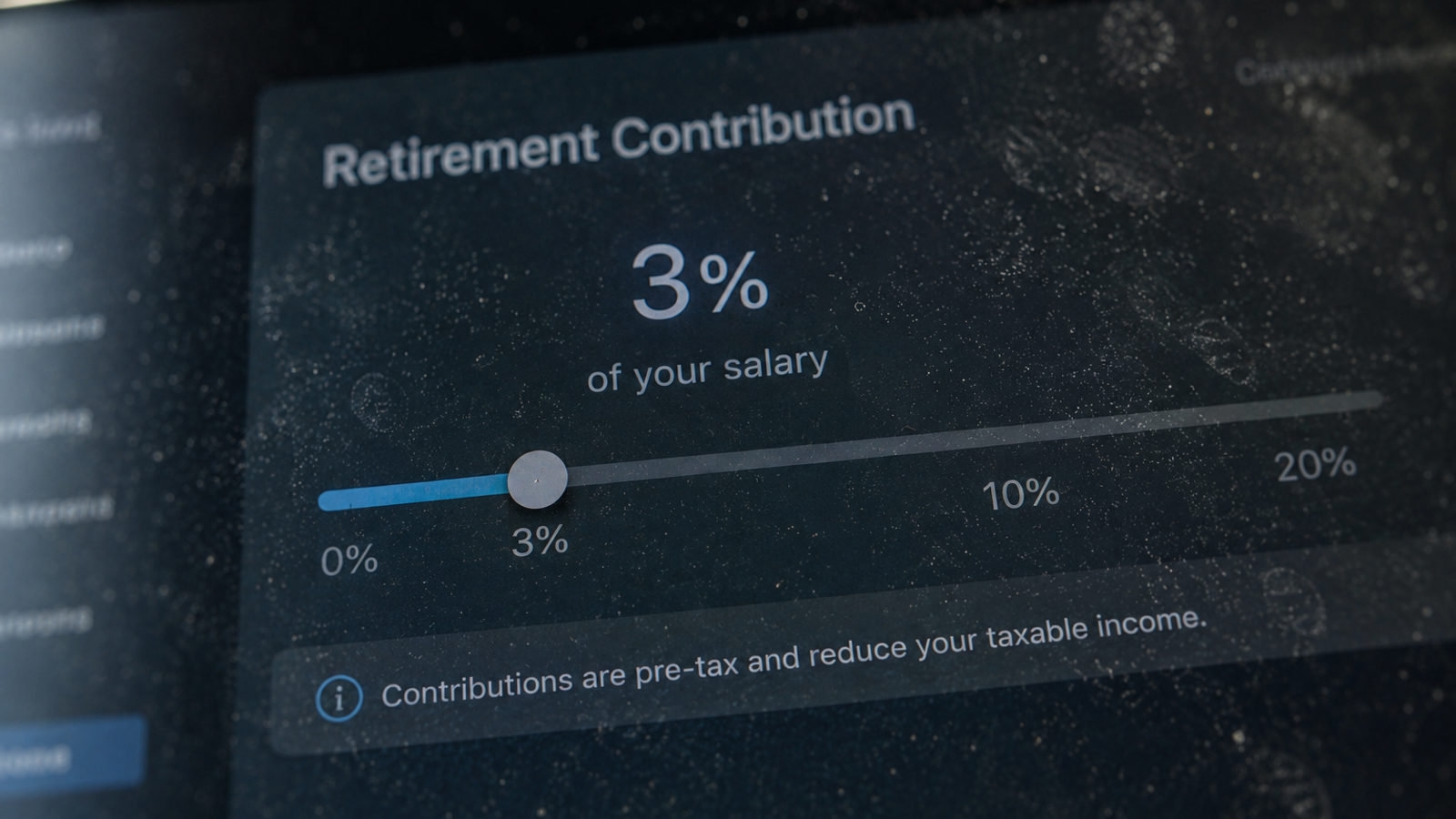

The 3% Problem

Default rates in auto-enrollment plans are often initially set very low, around 3%. Some plans now start at 6% or higher, but the legacy effect of 3% defaults persists across millions of accounts. The logic behind low defaults made sense to plan sponsors: set the bar low enough that nobody opts out. Maximize participation, minimize friction.

What plan sponsors underestimated—or perhaps understood but tolerated—was how effectively that 3% would function as an anchor. Not a floor, but a ceiling.

Employees interpret the default as a recommendation. If the company set it at 3%, that must be enough. Right?

It's not.

Fidelity's suggested combined 401(k) savings rate is 15%, which includes both employee contributions and employer match. The average 401(k) deferral rate in 2023 was an estimated 7.4%, and the average contribution rate registered at 6.5% in some recent studies. Even accounting for employer matches, most Americans are saving well below the recommended threshold.

The gap between 3% and 15% isn't a minor shortfall. Over a 30-year career, it's the difference between a comfortable retirement and working into your seventies.

The Math of Missed Opportunity

Let's work an example. A 30-year-old earning $60,000 a year contributes 3% to their 401(k). Their employer matches 50% of the first 6% of contributions, so they're getting an additional 1.5% in match (50% of their 3%). Total annual contribution: $2,700.

Now assume a 7% average annual return—reasonable for a diversified portfolio over three decades. By age 60, this worker has accumulated roughly $270,000.

Same worker, same salary, same match structure. But this time they contribute 10%. The employer still matches 50% of the first 6%, so the match goes up to 3%. Total annual contribution: $7,800. By age 60: approximately $780,000.

That's a $510,000 difference. For doing nothing more than adjusting a slider in an online portal.

The worker staying at 3% doesn't see this calculation. They see a steady accumulation. Their balance grows every year. It feels like progress. And it is—just dramatically insufficient progress.

Why Nobody Changes Anything

Behavioral economics explains the mechanism behind this inertia with uncomfortable precision.

Present bias: Humans discount future benefits steeply. A dollar today feels more real than ten dollars in 30 years, even when the math overwhelmingly favors the future. Retirement is abstract. A paycheck is concrete.

Loss aversion: Once households get used to a particular level of disposable income, they tend to view reductions in that level as a loss. Increasing your 401(k) contribution from 3% to 10% means your take-home pay drops. Even though you're not actually losing money—you're reallocating it to your future self—it feels like a loss now.

Status quo bias: The default option carries psychological weight beyond its numerical value. Changing it requires active decision-making, research, and a tolerance for uncertainty. Leaving it alone requires nothing.

The behavioral economics duo Richard Thaler and Shlomo Benartzi documented this dynamic in their foundational "Save More Tomorrow" research. They found that 78 percent of people who were offered the plan elected to use it, and virtually everyone (98 percent) who joined remained in it through two pay raises. The program worked by asking employees to commit now to increase savings rates later—specifically, when they got raises. The genius was in the timing: future commitment, not present sacrifice.

The average saving rates for participants increased from 3.5 percent to 11.6 percent over the course of 28 months. This wasn't magical. It was a direct application of behavioral insight: make the default work for inertia instead of against it.

The Target-Date Default

The second default—investment allocation—operates on similar principles but with less obvious costs.

Target-date funds are the most popular investment option used by 401(k) plan participants, and with assets nearing $5 trillion and adoption virtually universal, TDFs remain the primary engine of retirement savings for millions of participants. When you're auto-enrolled, your money almost certainly lands in a target-date fund matched to your projected retirement year.

TDFs are fine. In many cases, they're good. They offer automatic rebalancing, age-appropriate asset allocation, and a "set it and forget it" approach that works for people who don't want to become amateur portfolio managers.

But "fine" isn't "optimized." TDFs vary significantly in their glide paths—how aggressively they shift from stocks to bonds as you approach retirement. As COVID-19 disrupted financial markets in March 2020, TDFs that were further from their target dates lost a larger share of their value because they were more heavily invested in higher risk assets. An average TDF with a 2060 target date lost 14% in a single month, while a 2020 TDF lost 8%.

The point isn't that one fund is categorically better. It's that different funds have different risk profiles, fee structures, and performance histories, and most people never look at any of it. They land in the default and stay there.

Fees are particularly insidious. A difference of just one percentage point in fees (1.5% as compared with 0.5%) over 35 years dramatically affects overall returns. A worker with a $25,000 balance averaging 7% returns would have $227,000 at retirement with lower fees versus $163,000 with higher fees—a $64,000 haircut for doing absolutely nothing different except paying more in annual expenses.

The Policy Response

Regulators recognized the problem. The SECURE 2.0 Act, passed in December 2022, mandates that new 401(k) and 403(b) plans established after the passing of SECURE 2.0 must automatically enroll all eligible employees at a default contribution rate between 3 and 10% of their salary, with the most common default at 6%.

This is progress. Doubling the default from 3% to 6% meaningfully improves outcomes for workers who never touch their settings. But it's still a half-measure, because it doesn't address the core dynamic: defaults stick.

Automatic escalation—the practice of incrementally increasing contribution rates over time, typically tied to salary increases—offers a more elegant solution. Sixty-one percent of plans now default employees at a deferral rate of 4% or higher, up from 39% in 2014, and plans increasingly incorporate auto-escalation features.

The logic mirrors Save More Tomorrow: commit now to save more later. When your salary increases by 3%, your contribution rate ticks up by 1%. Your take-home pay still increases. You don't feel the loss. And over five years, you move from 6% to 11% without making a single active decision.

Yet auto-escalation remains optional for employers and inconsistently implemented. Many plans have escalation caps—stopping at 10% or 12% even though the recommended target is 15%. And crucially, employees can still opt out, which returns them to the land of active decision-making, where inertia often wins.

The Knowing-Doing Gap

Here's the uncomfortable part: most people know they should be saving more. Sixty-five percent of workers rank retirement as a priority. The information is available. Financial literacy campaigns abound. Calculators are free and ubiquitous.

And yet 59% of non-participants incorrectly thought they were already participating, with 49% of those mistakenly assuming they had been auto-enrolled.

The gap between knowing and doing isn't an information problem. It's a design problem.

We've built a retirement system that requires active, ongoing engagement in an area where most people have neither expertise nor interest. We've created dozens of decisions points—contribution rate, investment allocation, rebalancing frequency, Roth versus traditional, catch-up contributions—and then expressed surprise when people make none of them.

The default trap isn't a bug. It's a feature of a system designed for rational, engaged investors who will periodically review and optimize their accounts. The problem is that this describes almost no one.

What Actually Works

The solutions that work don't rely on education or willpower. They rely on better defaults.

Start higher: Plans that default new enrollees at 6% or higher see dramatically better outcomes than 3% plans. Some cutting-edge employers are starting at 10%. Workers rarely opt out, because the perceived recommendation anchors their expectation.

Auto-escalate aggressively: Gradual increases of 1-2% annually, capped at 15% rather than 10%, move people to adequate savings rates without triggering loss aversion. The increases happen after raises, so take-home pay continues to grow.

Make employer matches work harder: Rather than matching 50% of the first 6%, some employers match 100% of the first 3% and encourage higher contributions through tiered matching. The incentive structure reinforces good behavior.

Default to target retirement income, not target contribution rate: A few experimental plans flip the framing. Instead of "Save 10% of your salary," the default becomes "You'll need $60,000 a year in retirement. To get there, we recommend contributing X%." The behavioral response differs when the goal is concrete.

Charge opting out, not opting in: In a small number of pilot programs, employees who reduce their contribution rate below a plan-recommended threshold face a nominal administrative fee or mandatory consultation with a financial advisor. This doesn't prevent reduction—it just creates enough friction to interrupt pure inertia.

None of these are radical. They're incremental improvements to the architecture of choice, deployed in service of an outcome that everyone—workers, employers, regulators—agrees is desirable.

The Larger Question

The 401(k) was never designed to be the primary retirement vehicle for American workers. It emerged in 1978 as a tax-advantaged supplement to defined-benefit pensions. Then companies started terminating pension plans, and the 401(k) became the thing.

We've spent the last four decades retrofitting a supplemental savings account into a foundational pillar of retirement security, and the seams show. The default trap is one of them.

If we accept that most people won't actively manage their retirement accounts—and all available evidence suggests we should accept that—then the only responsible path forward is to make the defaults better. Not marginally better. Structurally better.

Higher starting rates. Aggressive auto-escalation with no caps below 15%. Investment options that prioritize low fees over plan administrator convenience. And perhaps most importantly, a cultural shift away from treating inaction as personal failure.

The worker who stays at 3% for 30 years isn't lazy. They're responding rationally to a system designed to exploit behavioral inertia for participation gains while tolerating catastrophic inertia on contribution rates. They're doing exactly what the default tells them to do.

The question isn't why they don't change. The question is why we built a system that requires them to.

The average 401(k) balance for someone in their 60s is around $304,200 for those who've been continuously enrolled for five years. Fidelity's benchmark for adequate retirement savings at that age: 10 times your salary. For someone earning $75,000, that's $750,000.

The gap is staggering. And for millions of Americans, it's the direct result of a single decision they never consciously made: accepting the default.